Sole Trader vs Limited Company UK: Which One Pays Less Tax in 2026?

Composed by Taxara on

22/6/2026

Choosing between being a sole trader or setting up a limited company is one of the biggest decisions for freelancers, contractors, consultants, and small business owners in the UK. The choice affects how much tax you pay, how much admin you deal with, how you take money from the business, and how protected you are if something goes wrong.

The simple answer is this: sole traders are usually simpler and often better for lower profits, while limited companies can be more tax-efficient for higher profits. But in 2026, the answer is not as clear-cut as it used to be because dividend tax rates have increased from 6 April 2026. HMRC shows dividend tax rates from 6 April 2026 as 10.75% for basic-rate taxpayers, 35.75% for higher-rate taxpayers, and 39.35% for additional-rate taxpayers.

Whichever structure you choose, managing your finances becomes much easier with the right tool. Taxara helps UK self-employed people and small business owners keep their income, expenses, invoices, and tax records in one place.

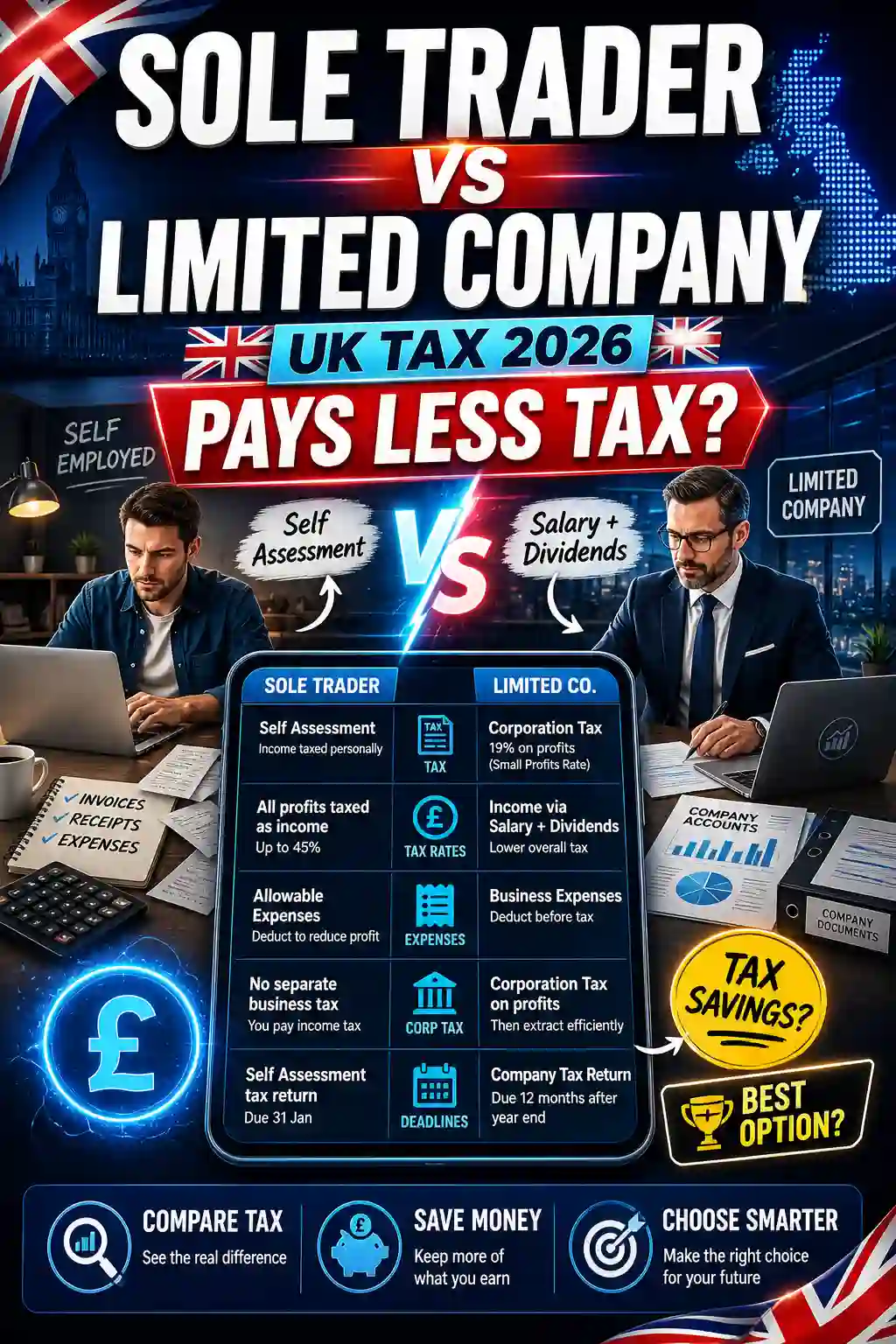

Sole Trader vs Limited Company: Quick Comparison

FactorSole TraderLimited CompanyLegal statusYou and the business are the sameThe company is a separate legal entityTax paidIncome Tax and National InsuranceCorporation Tax, then personal tax on salary or dividendsAdmin levelLowerHigherLiabilityPersonal liabilityLimited liabilityBest forFreelancers, side hustles, small businessesGrowing businesses, higher profits, formal clientsTax flexibilityLimitedMore flexibleSetupVery simpleRequires company registrationAccountsSelf AssessmentCompany accounts, Corporation Tax return, director filings

A sole trader keeps things simple. You earn money, deduct allowable business expenses, and pay tax on the profit. A limited company works differently. The company earns the money first, pays Corporation Tax, and then the director can take money through salary, dividends, or both.

How Sole Traders Are Taxed in the UK in 2026

A sole trader pays tax on profit, not total income. Profit means your business income minus allowable business expenses.

For example, if you earn £45,000 from clients and spend £8,000 on allowable business costs, your taxable profit is £37,000.

Sole traders usually pay:

Tax TypeWhat It Applies ToIncome TaxBusiness profit after expensesClass 4 National InsuranceSelf-employed profits above the thresholdVATOnly if registered or required to registerStudent loan repaymentsIf applicable

For the 2026/27 tax year, the standard UK Personal Allowance is £12,570, according to HMRC guidance. This means you can usually earn up to this amount before paying Income Tax, although the allowance reduces if your income is above £100,000. HMRC also confirms that the Personal Allowance reduces by £1 for every £2 of adjusted net income above £100,000.

Sole traders also need to keep proper records of income and expenses. This is becoming even more important because Making Tax Digital changes how many self-employed people report income to HMRC. You can also read more about HMRC’s MTD rules for small business owners if you want a clearer breakdown.

Main Benefits of Being a Sole Trader

The biggest benefit of being a sole trader is simplicity. You do not need to register a company, file company accounts, or deal with Corporation Tax. You usually only need to register as self-employed, keep accurate records, and submit a Self Assessment tax return.

For many people, this is enough. If you are a freelancer, delivery driver, tutor, designer, tradesperson, consultant, or side-hustle owner, sole trader status can be the easiest way to start.

Another benefit is cost. Accountancy fees are usually lower for sole traders because the reporting requirements are simpler. This matters because a limited company may save tax in some cases, but those savings can disappear if admin and accountancy costs are high.

Main Downsides of Being a Sole Trader

The main downside is personal liability. As a sole trader, there is no legal separation between you and the business. If the business owes money, has a legal dispute, or faces a claim, your personal assets may be at risk.

Sole traders also have less flexibility in tax planning. All profits are treated as your personal income in the tax year they are earned. You cannot leave profits inside the business in the same way a limited company can.

When Sole Trader Status May Be Better

Sole trader status may be better if:

SituationWhy Sole Trader May WorkYour profit is lowTax savings from a company may be too smallYou want simple adminSelf Assessment is easier than company accountsYou take all profits personallyA company gives less benefit if you withdraw everythingYou are testing a business ideaSimple setup makes it easier to startYou want lower accounting costsSole trader accounts are usually cheaper

If you are leaning toward staying self-employed, this guide on choosing the best tax app for sole traders is a useful next step.

How Limited Companies Are Taxed in the UK in 2026

A limited company is a separate legal entity. This means the company earns income, pays expenses, owns assets, and pays Corporation Tax on its profits.

For 2026, HMRC lists the small profits Corporation Tax rate as 19% for companies with profits under £50,000 and the main rate as 25% for companies with profits over £250,000. Marginal Relief may apply between £50,000 and £250,000.

Company ProfitCorporation Tax PositionUp to £50,00019% small profits rate£50,001 to £250,000Marginal Relief may applyOver £250,00025% main rate

After the company pays Corporation Tax, the director can take money out of the company. This is usually done through salary, dividends, or a mix of both.

Salary vs Dividends

A salary is paid through payroll. It is usually an allowable company expense, which can reduce company profit before Corporation Tax. However, salary may create Income Tax and National Insurance responsibilities.

Dividends are different. They are paid from company profits after Corporation Tax. Dividends do not attract National Insurance, but they are taxed personally when received above the dividend allowance.

From 6 April 2026, dividend tax rates are:

Tax BandDividend Tax RateBasic rate10.75%Higher rate35.75%Additional rate39.35%

HMRC says the ordinary and upper dividend tax rates increased by 2 percentage points from April 2026, while the additional rate stayed at 39.35%. This matters because limited companies have often been seen as more tax-efficient due to the salary-dividend mix. In 2026, that advantage may still exist for some business owners, but it needs to be calculated carefully.

Sole Trader vs Limited Company: Which Pays Less Tax?

There is no single answer because the best structure depends on profit, expenses, personal income needs, and long-term plans. But there are some useful patterns.

Lower Profits

At lower profit levels, a sole trader is often the better choice. The tax may be similar, but the admin is much lighter. You avoid company filing requirements, payroll complexity, director responsibilities, and higher accountancy fees.

If you are earning under £30,000 profit, a limited company may not create enough tax savings to justify the extra work.

Medium Profits

Between around £30,000 and £50,000 profit, the decision becomes more balanced. Some people still prefer sole trader status because it is simple. Others may choose a limited company for liability protection, professional image, or future growth.

At this stage, tax should not be the only deciding factor. You should also think about whether you want to retain profits, hire staff, work with larger clients, or build a more formal business.

Higher Profits

At higher profit levels, a limited company may become more attractive. This is especially true if you do not need to withdraw all the money personally.

For example, if your company makes £90,000 profit and you only need £45,000 for personal living costs, the remaining profit can potentially stay inside the company after Corporation Tax. That retained money can be used for business growth, equipment, marketing, hiring, or future investment.

A sole trader does not get the same flexibility because profits are taxed personally in the year they are earned.

Profit LevelLikely Better OptionReasonUnder £30,000Sole traderSimple and low admin£30,000–£50,000DependsTax savings may be limited£50,000–£100,000Limited company may helpMore tax planning flexibility£100,000+Limited company often worth reviewingPersonal Allowance taper and retained profits matter more

Admin Burden: Which Is Easier to Manage?

A sole trader has less admin. You keep records, track expenses, and submit a tax return. A limited company has more duties, including company accounts, Corporation Tax returns, payroll if taking salary, confirmation statements, and director responsibilities.

This is why admin cost should be included in the decision. Saving £800 in tax is not very useful if you spend £1,200 more on accounting and lose more time managing paperwork.

Whichever route you take, automated bookkeeping can remove much of the day-to-day burden by tracking income, expenses, invoices, and tax records automatically.

Whether you are a sole trader or company director, you can also manage it all from your phone, which is useful if you work with clients, travel often, or manage finances outside normal office hours.

Limited Company Benefits Beyond Tax

A limited company is not just about tax. It can also make your business look more established.

Some agencies, corporate clients, and larger companies prefer working with limited companies. A company structure can also help if you want to bring in shareholders, hire employees, sell the business later, or separate business risk from your personal life.

Limited liability is another major benefit. In most cases, the company is responsible for its debts, not you personally. This protection is not unlimited, especially if there is fraud, personal guarantees, or director misconduct, but it is still a key reason many business owners incorporate.

Professional invoicing also becomes more important when operating through a company. Your invoices should include the correct company name, registration details, payment terms, and VAT details if registered. If invoicing is becoming a regular part of your work, this guide on an invoicing app for freelancers may also help.

So, Which One Pays Less Tax in 2026?

If your business is small, simple, and you take all the money out for personal use, being a sole trader may cost less overall. The tax may not be much higher, and you avoid the extra admin and accountancy fees of running a company.

If your business earns higher profits, carries more risk, or you want to retain money in the business, a limited company may be more tax-efficient and more practical. But because dividend tax rates increased from April 2026, the company route should be reviewed carefully before assuming it saves money.

The best answer is:

If You WantConsiderSimplicitySole traderLower admin costsSole traderLimited liabilityLimited companyTax planning flexibilityLimited companyRetaining profitsLimited companyTesting a new ideaSole traderScaling a businessLimited company

What Should You Do Next?

Before changing your structure, look at your expected profit, how much money you need personally, your business risks, and your admin costs. A UK accountant can help you compare the real numbers for your situation. For product-related questions, you can also contact Taxara directly.

You should also think about the software and tools you will use. Good bookkeeping matters whether you are self-employed or running a company. Taxara’s straightforward pricing makes it easier to understand your monthly cost without guessing what support will cost later.

You can also read the story behind Taxara to understand why the app was built for UK small business owners.

Final Verdict

A sole trader can be the better choice for lower-profit businesses because it is simple, affordable, and easy to manage. A limited company can be better for higher-profit businesses because it offers more tax planning flexibility, limited liability, and a more formal business structure.

In 2026, the winner depends on your profit level and how you take money from the business. Do not choose a limited company only because someone says it always saves tax. It does not. Run the numbers, understand the admin, and choose the structure that fits your business.

Ready to simplify your tax and bookkeeping? Try Taxara free.

Never stress again

Never be late again

Never waste time

On time.

In shape.

Taxara keeps your finances in shape and always on time - with just a few simple taps and clicks.

Try for free

Simple.

Affordable.

Taxara comes with a free plan, and the premium one starts from £6.99 - about the same as your daily coffee.

Try for free

Your time.

All yours.

Win back your time and focus on what you love most - let Taxara’s AI take care of the rest.

Try for freeGot questions?

Save time for what matters most - with Taxara

Taxara Ltd. 273/275 Wilmslow Road, Manchester, England

info@taxara.co.uk

support@taxara.co.uk

.png)

.png)

.png)